Documents

Poster

Poster

Unsupervised learning of asymmetric high-order autoregressive stochastic volatility model

- Citation Author(s):

- Submitted by:

- Ivan Gorynin

- Last updated:

- 7 March 2017 - 6:12am

- Document Type:

- Poster

- Document Year:

- 2017

- Event:

- Presenters:

- Ivan Gorynin

- Paper Code:

- ICASSP1701

- Categories:

- Log in to post comments

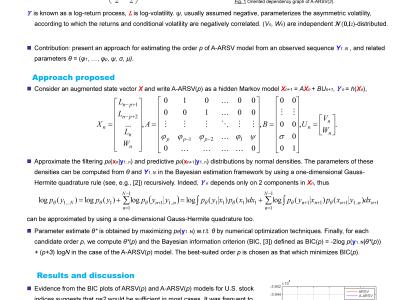

We introduce a new estimation algorithm specifically designed for the latent high-order autoregressive models. It implements the concept of the filter-based maximum likelihood. Our approach is fully deterministic and is less computationally demanding than the traditional Monte Carlo Markov chain techniques. The simulation experiments confirm the interest of our approach.